The pursuit of passive income has become a common financial goal for millions of Americans. With inflation concerns, economic uncertainty, and a growing desire for financial independence, investors are looking for ways to generate returns without constant attention. This guide explores the most effective passive income investments available today, examining their potential returns, risk profiles, and suitability for different investor profiles.

Understanding the current market landscape matters before committing capital. Interest rates have stabilized after the aggressive hiking cycle of 2022-2023, creating new opportunities in fixed-income products. Meanwhile, the stock market continues its long-term upward trajectory, and real estate remains a cornerstone of wealth-building strategies. The key is selecting investments that align with your risk tolerance, time horizon, and financial objectives.

What to Look for in Passive Income Investments

Before exploring specific opportunities, you should understand what makes a passive income investment worth holding. These factors determine whether an investment will deliver consistent returns while minimizing downside risk.

Cash Flow Consistency is the primary consideration for passive income investors. The best investments generate regular, predictable distributions rather than relying solely on capital appreciation. Dividend-paying stocks, rental properties, and interest-bearing accounts provide this stability, though each carries different risk characteristics.

Risk Assessment must factor into every investment decision. Passive income investments generally range from low-risk, lower-return options like high-yield savings accounts to higher-risk ventures with greater income potential. Understanding your personal risk tolerance helps you avoid costly mistakes during market volatility.

Liquidity matters significantly for investors who may need to access their capital quickly. Some passive income investments, such as real estate, require substantial holding periods and carry penalties for early withdrawal. Others, like publicly traded stocks and ETFs, offer daily liquidity with minimal transaction costs.

Minimum Investment Requirements vary dramatically across asset classes. Understanding these thresholds helps you allocate resources appropriately and avoid overconcentration in illiquid positions. The rise of fractional shares and low-minimum investment platforms has opened up many previously exclusive opportunities.

Tax Implications significantly impact net returns. Qualified dividends receive preferential tax treatment, while ordinary income from certain investments faces higher tax rates. Consulting with a tax professional helps you maximize after-tax returns rather than focusing solely on pre-tax yields.

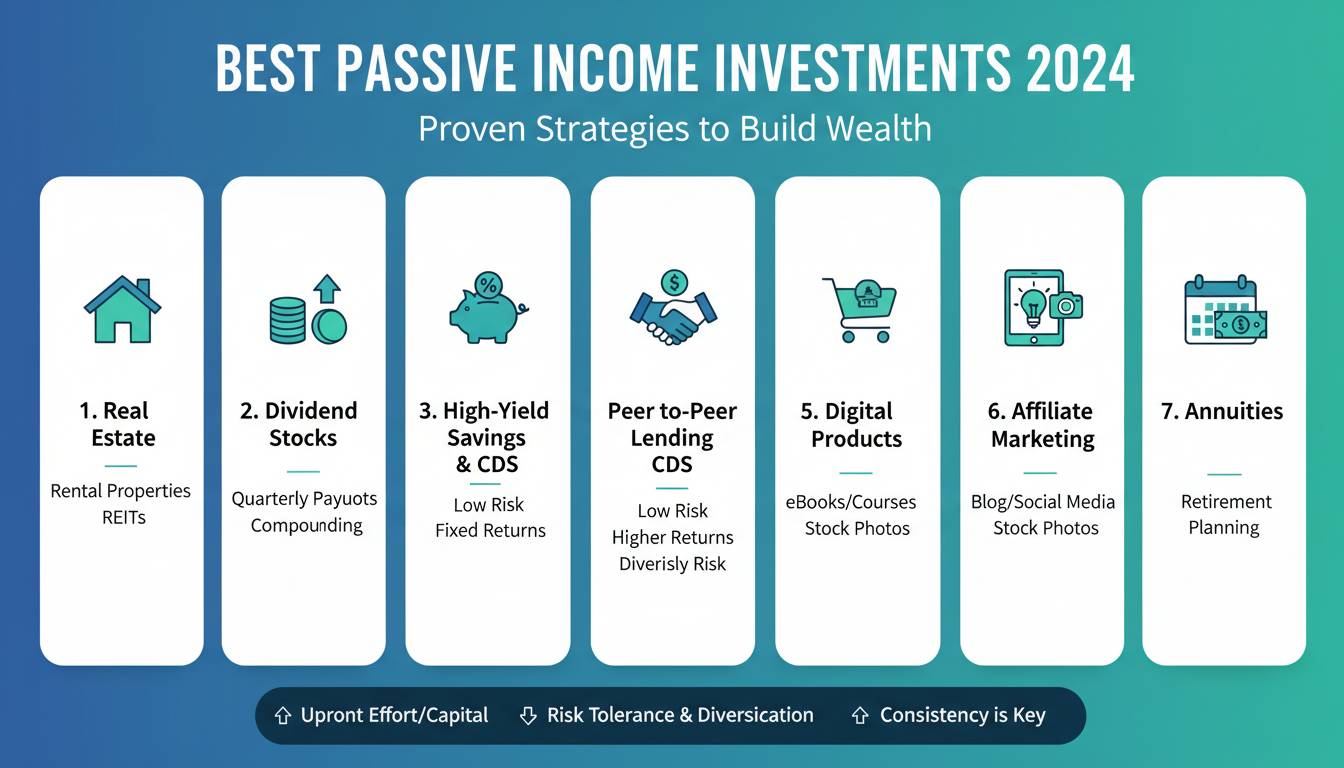

Top Passive Income Investments for 2024

The following investment options represent the most compelling opportunities for generating passive income in the current market. Each category offers distinct advantages and considerations for different investor profiles.

Dividend Stocks

Dividend stocks remain a staple in many passive income portfolios. Companies that consistently pay and grow their dividends have demonstrated financial strength. The S&P 500 dividend aristocrats, companies that have increased dividends for at least 25 consecutive years, represent particularly reliable income sources.

Blue-chip dividend stocks from established companies in sectors like utilities, consumer staples, and healthcare typically offer yields between 2% and 5%. These sectors maintain stable cash flows even during economic downturns, supporting continued dividend payments. Companies like Johnson & Johnson, Procter & Gamble, and ExxonMobil exemplify this defensive characteristic.

The key advantage of dividend stocks is their potential for both income and growth. While you receive regular cash distributions, the underlying stock value can appreciate over time, creating total returns that exceed simple yield calculations. Reinvesting dividends through dividend reinvestment programs (DRIPs) compounds returns exponentially over extended periods.

Real Estate Investment Trusts (REITs)

Real Estate Investment Trusts provide a way to access commercial real estate without the complexities of direct property ownership. REITs own and operate income-producing properties, distributing at least 90% of taxable income to shareholders as dividends. This structure delivers significant tax advantages while providing consistent income streams.

The REIT sector encompasses diverse property types, including office buildings, shopping centers, residential complexes, warehouses, and data centers. This diversification reduces concentration risk while exposing investors to different real estate market segments. Healthcare REITs and industrial REITs have shown particular resilience in recent years.

Annual dividend yields for quality REITs typically range from 3% to 7%, depending on property type and leverage levels. Mortgage REITs, which finance real estate rather than owning properties, often offer higher yields but carry additional interest rate sensitivity. You should evaluate REIT dividend sustainability by examining funds from operations (FFO) coverage ratios.

High-Yield Savings Accounts and Money Market Funds

The Federal Reserve’s interest rate increases from 2022 through 2023 have transformed high-yield savings accounts from negligible contributors to meaningful passive income sources. Online banks and credit unions now offer savings rates exceeding 4.5% annually, significantly outperforming traditional brick-and-mortar institutions.

Money market funds provide another option for cash allocations, typically offering slightly higher yields than savings accounts while maintaining strong liquidity. These funds invest in short-term government securities and commercial paper, preserving capital while generating modest income. The yields on money market funds fluctuate daily in response to prevailing interest rates.

While these cash alternatives won’t build significant wealth independently, they serve crucial roles in portfolio construction. They provide emergency fund reserves, opportunity capital for future investments, and stability during market downturns. The near-zero risk of principal loss makes them essential components of any diversified investment strategy.

Index Funds and Exchange-Traded Funds (ETFs)

Index funds and ETFs offer passive income through diversification and low costs. Dividend-focused index funds, which track indexes of high-dividend-paying stocks, provide broad market exposure while generating regular income distributions. The expense ratios on index funds are typically under 0.10%, minimizing the drag on returns.

Target-date funds automatically adjust asset allocation as you approach retirement, shifting from growth-oriented positions to income-generating assets. This hands-off approach suits investors seeking passive income without managing individual position allocations.

ETFs offer additional flexibility through strategies like covered call writing, which generates option premium income in exchange for limiting upside potential. While these strategies add complexity, they can enhance yield in flat or modestly trending markets. Income-focused ETFs have attracted significant investor capital in 2024 as the search for yield intensifies.

Rental Properties

Direct real estate ownership remains one of the most time-tested methods for generating passive income. Rental properties provide monthly cash flow while building equity through mortgage amortization and property appreciation. The tax advantages, including depreciation deductions and potential 1031 exchange eligibility, further enhance after-tax returns.

The rise of property management companies has made rental ownership more genuinely passive than in previous generations. Professional managers handle tenant screening, maintenance, rent collection, and legal compliance, for a percentage of rental income. This arrangement reduces but does not eliminate your involvement in property decisions.

Location remains the paramount consideration for rental property investment. Markets with strong job growth, population increases, and limited new construction supply tend to sustain rental demand and price appreciation. Secondary and tertiary markets often offer better cap rates than major coastal cities, though with potentially lower long-term appreciation potential.

Bonds and Fixed Income Securities

Individual bonds and bond funds provide predictable income streams through regular interest payments. Treasury bonds, corporate bonds, and municipal bonds each offer different yield and risk characteristics. The income from municipal bonds often receives favorable tax treatment, enhancing after-tax yields for investors in higher tax brackets.

Bond yields have become more attractive following the rate-hiking cycle. Investment-grade corporate bonds now offer yields approaching 5% to 6%, while Treasury securities provide safe yields exceeding 4% for longer maturities. This income level rivals historical equity returns while carrying significantly lower volatility.

Bond ladders represent a sophisticated fixed-income strategy for income-focused investors. By purchasing bonds with staggered maturity dates, you create rolling income streams while maintaining liquidity for reinvestment at prevailing rates. This approach reduces interest rate risk by continuously reinvesting at current market yields.

Peer-to-Peer Lending

Peer-to-peer platforms connect individual lenders directly with borrowers, eliminating traditional financial institution intermediation. These platforms typically offer yields ranging from 4% to 10%, depending on borrower credit quality and loan terms. The higher yields compensate lenders for assuming default risk.

The primary advantage of peer-to-peer lending is customizable risk-return profiles. You can select loan grades matching your risk tolerance, from high-yield, higher-risk loans to conservative, lower-yield options. Diversifying across many loans reduces the impact of individual borrower defaults on overall portfolio returns.

Platform selection matters significantly in peer-to-peer investing. Established platforms with longer track records, robust credit assessment methodologies, and strong recovery processes tend to deliver better long-term results. You should examine historical default rates, platform fees, and liquidity provisions before committing capital.

How to Choose the Right Passive Income Investment

Selecting among passive income opportunities requires honest assessment of your individual circumstances and objectives. No single investment suits all investors, and optimal portfolios typically combine multiple income streams to balance risk, return, and liquidity considerations.

Time Horizon significantly influences appropriate investment selections. If you have decades until retirement, you can tolerate higher volatility and should emphasize growth-oriented investments like dividend stocks and REITs. Those approaching or in retirement require more stable income sources and may favor bonds, high-yield savings, and conservative dividend payers.

Risk Tolerance varies widely among investors and should drive asset allocation decisions. Some individuals experience sleepless nights during market downturns, suggesting a more conservative approach despite potentially lower long-term returns. Others view volatility as opportunity, allowing more aggressive positioning.

Income Requirements determine how much passive income you need from your portfolio. If you require substantial annual distributions, you must accept higher withdrawal rates, potentially impacting portfolio longevity. Lower income requirements allow more conservative positioning and greater long-term sustainability.

Account Type affects investment selection through tax implications. Roth IRAs and 401(k)s offer tax-advantaged environments where high-yielding investments can grow without immediate tax consequences. Taxable accounts benefit from investments with qualified dividend treatment or municipal bond eligibility.

Diversification Across Multiple Passive Income Streams reduces portfolio risk while enhancing overall income stability. Relying on a single income source creates vulnerability to sector-specific challenges. A balanced approach combining dividend stocks, REITs, bonds, and cash equivalents provides multiple income pillars that sustain through various market conditions.

Frequently Asked Questions

What is the best passive income investment for beginners?

For beginners, high-yield savings accounts and dividend reinvestment plans (DRIPs) through low-cost index funds offer the most accessible entry points. High-yield savings provide guaranteed returns with zero risk, while index funds offer diversification and historically strong returns with minimal expertise required. Starting with these simpler vehicles allows you to learn market dynamics before exploring more complex investments like rental properties or peer-to-peer lending.

How much money do I need to start generating passive income?

The minimum investment varies significantly by asset class. High-yield savings accounts often require no minimum deposit, while index funds can be started with the price of a single share or even fractional shares through many brokerages. REITs and individual dividend stocks typically require several hundred dollars to start. Rental properties require substantially more capital, often $50,000 or more when accounting for down payments, closing costs, and initial reserves.

Are passive income investments risky?

All investments carry some degree of risk, but passive income investments span a wide risk spectrum. High-yield savings accounts and Treasury securities carry virtually no risk of principal loss. Dividend stocks and REITs carry market risk and can decline in value during economic downturns. Rental properties face vacancy risk, maintenance costs, and property value fluctuations. The key is matching investments to appropriate risk tolerance rather than avoiding risk entirely.

How do dividends generate passive income?

Dividends represent cash payments that companies make to shareholders from their profits. When you own dividend-paying stocks or funds, you receive regular payments, typically quarterly, based on the number of shares you own. The dividend yield is calculated by dividing the annual dividend payment by the stock price, expressed as a percentage. Reinvesting dividends purchases additional shares, accelerating portfolio growth through compounding.

What is a good passive income yield in 2024?

A good passive income yield depends on current market conditions and risk considerations. High-yield savings accounts offer around 4.5% with minimal risk. Investment-grade bonds yield approximately 5% to 6%. Dividend stocks typically yield 2% to 4%, while REITs often yield 4% to 7%. The highest yields generally carry elevated risk, so you should evaluate sustainability rather than pursuing maximum yields alone.

How can I create passive income without a lot of money?

Starting small with fractional shares in index funds allows beginning investors to build wealth gradually. Automatic contributions, even modest ones, compound significantly over time through dollar-cost averaging. High-yield savings accounts require no minimum for many online banks. Additionally, developing marketable skills that generate royalty income—such as writing, photography, or software development—requires minimal capital but substantial upfront effort.

Conclusion: Building Your Passive Income Portfolio in 2024

The landscape for passive income investments in 2024 offers compelling opportunities across multiple asset classes. From the stability of high-yield savings to the growth potential of dividend stocks and the tangible benefits of real estate, investors have more options than ever to build wealth through passive means.

Success in passive income investing requires patience, diversification, and realistic expectations. No investment delivers truly effortless returns, and all carry some degree of risk. The most sustainable approach combines multiple income streams appropriate for your individual circumstances, time horizon, and risk tolerance.

Starting early remains the most powerful wealth-building strategy available. Compound interest works exponentially over time, meaning the difference between beginning at age 25 versus age 35 can represent hundreds of thousands of dollars in eventual portfolio value. The best time to begin investing was yesterday; the second-best time is today.

As you construct your passive income portfolio, remember that markets fluctuate, economic conditions evolve, and investment opportunities shift. Maintaining a long-term perspective, regularly reviewing your allocations, and staying informed about changing market dynamics will position you to achieve financial independence through passive income generation.