Introduction

High-yield savings accounts have become worth considering in 2024 as interest rates finally give savers a decent return. Traditional banks still offer almost nothing—often less than 0.01% APY—while online banks advertise rates above 5%. The difference adds up fast.

This guide covers what’s available, which accounts are worth your time, and how to pick the right one. Rates have climbed dramatically since 2022, and while they’ve stabilized somewhat, savers today can still earn meaningful interest without much effort.

Understanding High-Yield Savings Accounts

A high-yield savings account is exactly what it sounds like: a savings account that pays more interest. Online banks and credit unions offer them because they don’t have the overhead of branch networks, so they pass those savings to customers.

Here’s why it matters. Put $10,000 in a typical brick-and-mortar savings account earning 0.01%—you get $1 per year. That same $10,000 at 5% APY gets you roughly $500. That’s not life-changing money, but it’s also not nothing. The gap widens with larger balances.

These accounts are FDIC-insured up to $250,000, same as regular savings. You get six withdrawals per statement cycle under federal rules, and most banks don’t impose anything unusual beyond that. Minimum deposits vary—some accounts require nothing to open, others want $100 or more.

Current Market Rates and Trends in 2024

Rates in 2024 sit between 4.25% and 5.25% at the most competitive online banks. That’s far better than what you’d get at Chase or Bank of America, though it’s come down slightly from the peaks seen in 2022 and 2023.

Why the difference? Online banks have lower costs. They don’t maintain thousands of branches or employ as many people. Credit unions can also offer competitive rates since they’re member-owned, though you’ll need to qualify for membership.

Promotional rates exist—you’ll see banks advertise higher APYs for the first few months to attract new customers. Just know that the rate drops after the promo period ends. Always check the ongoing rate, not just the teaser.

Methodology: How We Selected the Best Accounts

We looked at a few things:

- APY: Both the promotional rate and what you get after it ends

- Minimum deposit: Whether you need money up front to open the account

- Fees: Monthly maintenance fees, withdrawal fees, and anything else that eats into your returns

- Platform quality: How well the website and app work

- Customer service: Whether you can actually reach someone when something goes wrong

Rate matters, but it’s not everything. A bank with a slightly lower rate but no fees might actually save you money.

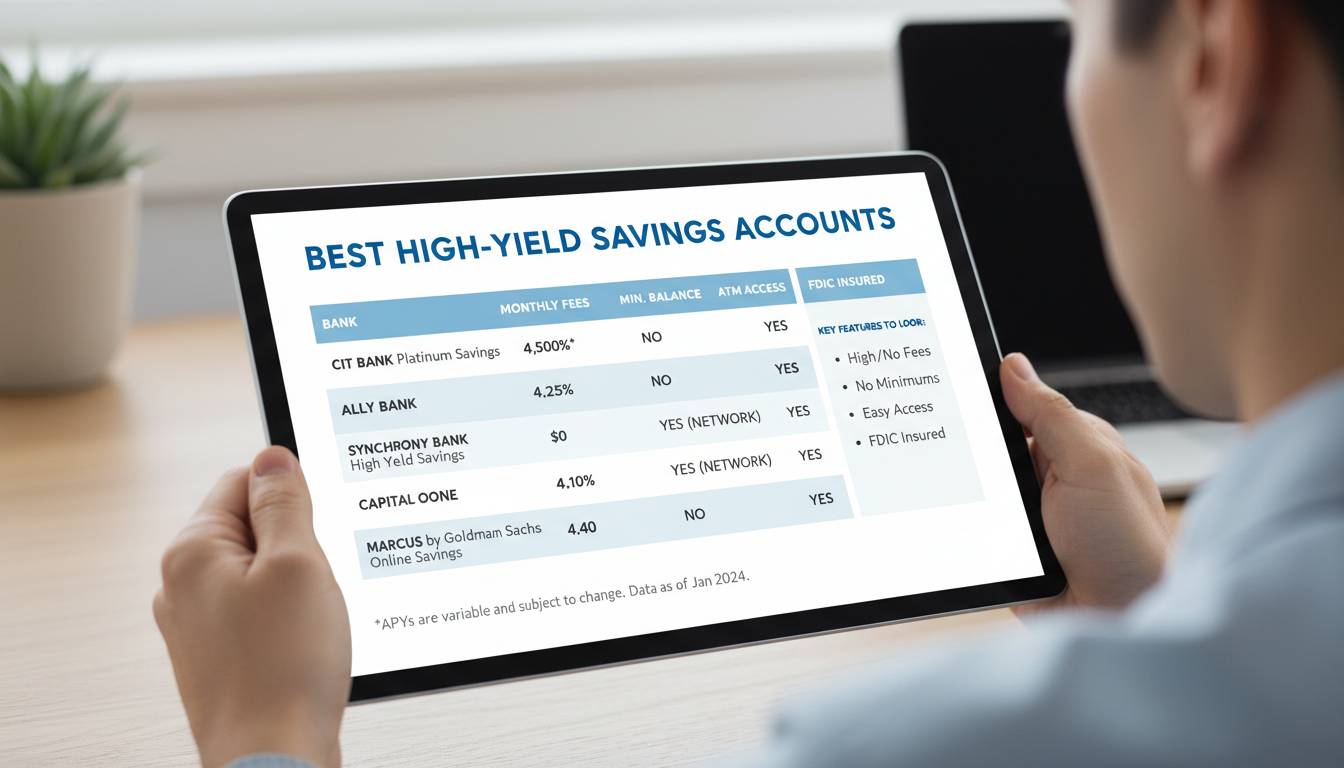

Top High-Yield Savings Accounts of 2024

| Bank/Institution | APY | Minimum Deposit | Monthly Fee | Key Features |

|---|---|---|---|---|

| CIT Bank | 4.85% | $100 | $0 | Higher rate tier available |

| Ally Bank | 4.25% | $0 | $0 | 10 sub-accounts for tracking goals |

| Marcus by Goldman Sachs | 4.40% | $0 | $0 | Simple, no-frills approach |

| Discover Bank | 4.30% | $0 | $0 | Rewards program |

| American Express National Bank | 4.35% | $0 | $0 | Good mobile app |

| Synchrony Bank | 4.75% | $0 | $0 | Large ATM network |

| Capital One | 4.25% | $0 | $0 | Well-known brand |

Each has strengths. CIT Bank pays more if you can meet the $100 minimum. Ally is good if you want to split savings into separate buckets. Marcus has a solid reputation for actually answering the phone when you call.

Features to Look for in a High-Yield Savings Account

Fee structure is the first thing to check. Some accounts charge $10 or $15 per month if your balance drops below a certain threshold. Others are genuinely free. Those fees quietly eat up your interest gains.

Mobile banking matters more than people admit. You probably won’t visit a branch for a savings account—you’ll use an app. If it’s clunky or crashes, you’ll hate keeping money there.

Customer service is one area where online banks vary wildly. Some let you chat with someone in minutes. Others make you wait on hold for 45 minutes or worse. This becomes important the one time you have a problem.

Sub-accounts let you organize money for different goals—emergency fund, vacation, car savings. Nice to have, not essential.

Pros and Cons of High-Yield Savings Accounts

Pros:

- Interest rates beat traditional savings by a wide margin

- FDIC insurance protects your money

- Online banking is convenient

- Most accounts have no minimum deposit

Cons:

- Rates are variable—they go up, but they also go down

- No rate lock like you’d get with a CD

- You won’t get in-person service (unless you care about that)

- You might need to switch banks occasionally to get the best rate

How to Open a High-Yield Savings Account

The process takes about 10 minutes online. You’ll provide your name, address, Social Security number, and bank account information to fund the initial deposit.

Funding options include ACH transfer from your existing bank (usually one to three business days), wire transfer (faster but may cost fees at the sending bank), or mailing a check (slowest).

Once open, set up automatic transfers from your checking account. Saving consistently beats saving sporadically, and automation removes the “I’ll do it later” problem.

Conclusion

High-yield savings accounts aren’t exciting, but they work. Moving money from a bank paying 0.01% to one paying 4% or 5% is an easy win with zero risk. You’ll earn more interest without doing anything differently.

The accounts listed above are legitimate options. Pick one with no monthly fees and a rate that competes. Set up automatic deposits and forget about it.

One caveat: rates will probably come down eventually. Enjoy them while they last.

Frequently Asked Questions

What is a high-yield savings account?

A savings account that pays significantly more interest than traditional accounts. Online banks and credit unions offer them. APYs typically range from 4% to 5%.

Are high-yield savings accounts safe?

Yes, if the bank is FDIC-insured. Your deposits are protected up to $250,000 per account ownership category. The federal government backs this insurance.

What is the minimum deposit required?

Many require $0. Some want $100 or more. Most leading online banks now offer no-minimum options.

How often do rates change?

Any time. These are variable-rate accounts. Banks adjust based on Federal Reserve policy and market conditions. Unlike CDs, there’s no guarantee.

Can I have multiple high-yield savings accounts?

Absolutely. Many people do. Just make sure each account is at a different institution if you want full FDIC coverage above $250,000.

How do they compare to money market accounts?

Similar—both are FDIC-insured and offer competitive rates. Money market accounts sometimes include limited check-writing. Savings accounts are simpler. Either works for short-term goals.